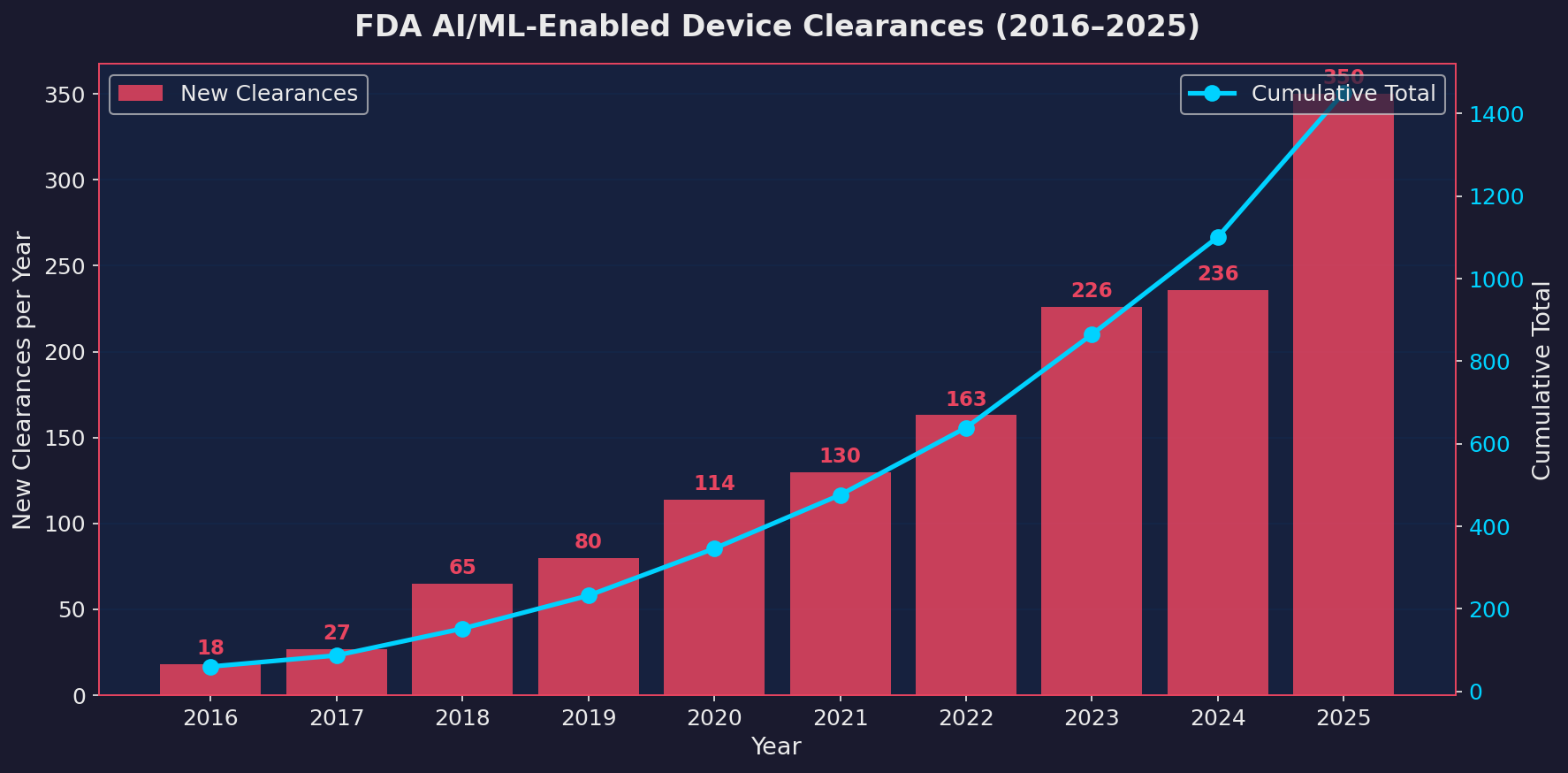

I downloaded the FDA’s complete list of AI/ML-enabled medical devices today. 1,451 devices, dating back to 1995.

In 2025, the FDA cleared 350 devices with some form of machine learning built in. That’s a 48% jump from 2024’s 236. To put it in perspective, the entire period from 1995 to 2019, twenty-four years, produced 309 total clearances. 2025 alone beat that in twelve months.

Here’s the big picture. From 2016 to 2020, the numbers were growing but manageable. Then 2021 onwards, the curve steepened. 2024 looked like a plateau year with only 4.4% growth. Some people thought the market was saturating. Then 2025 happened.

| Year | New Clearances | Year-over-Year Growth |

|---|---|---|

| 2018 | 65 | +140.7% |

| 2019 | 80 | +23.1% |

| 2020 | 114 | +42.5% |

| 2021 | 130 | +14.0% |

| 2022 | 163 | +25.4% |

| 2023 | 226 | +38.7% |

| 2024 | 236 | +4.4% |

| 2025 | 350 | +48.3% |

That 2024 slowdown looks like it was a speed bump, not a ceiling. My guess is that the backlog from 2023’s submission surge plus an influx of new applications from smaller companies created the 2025 wave. But the structural story is clear: more companies are building LLM and machine learning features into medical devices every year, and the pace is accelerating.

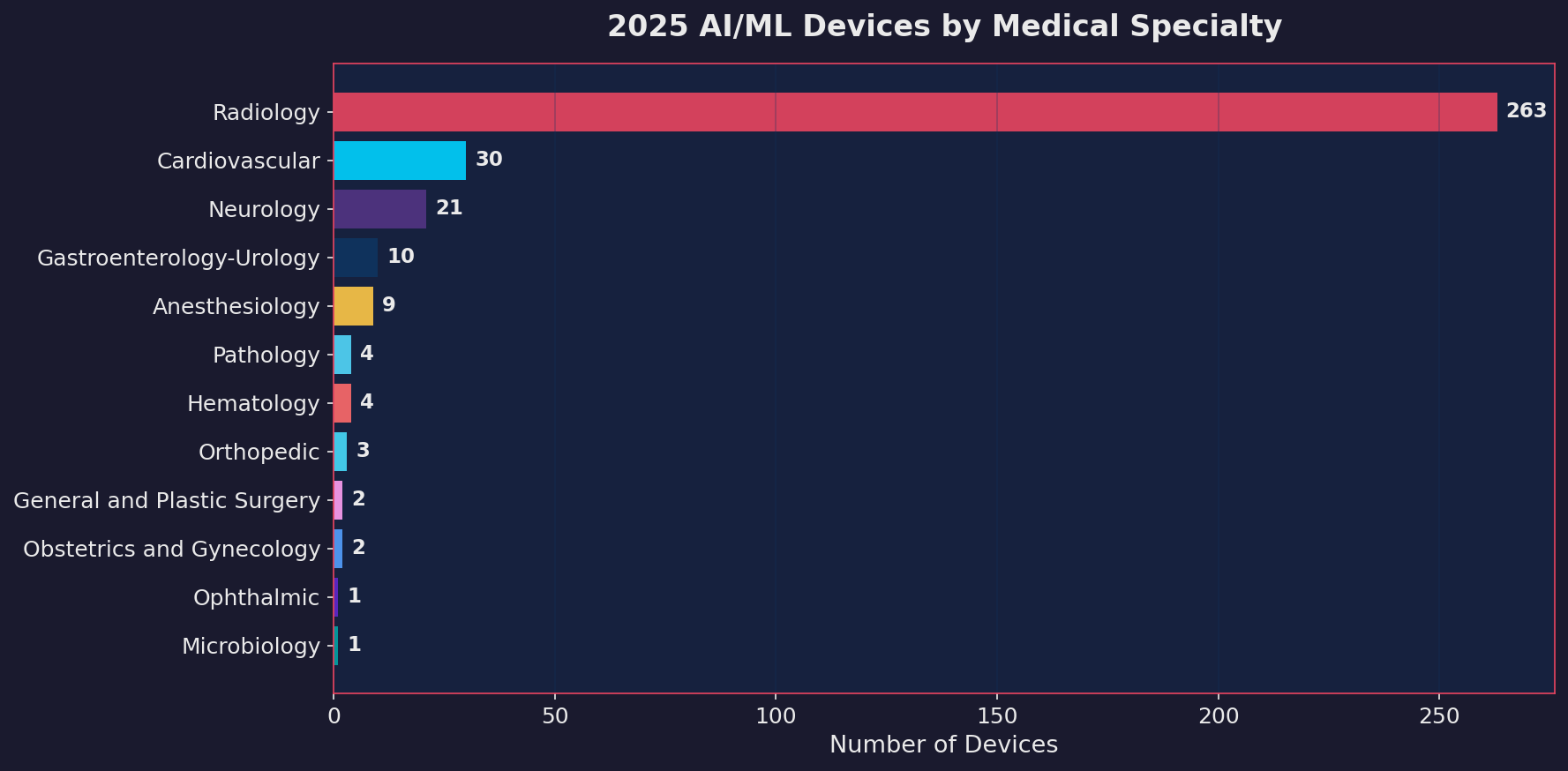

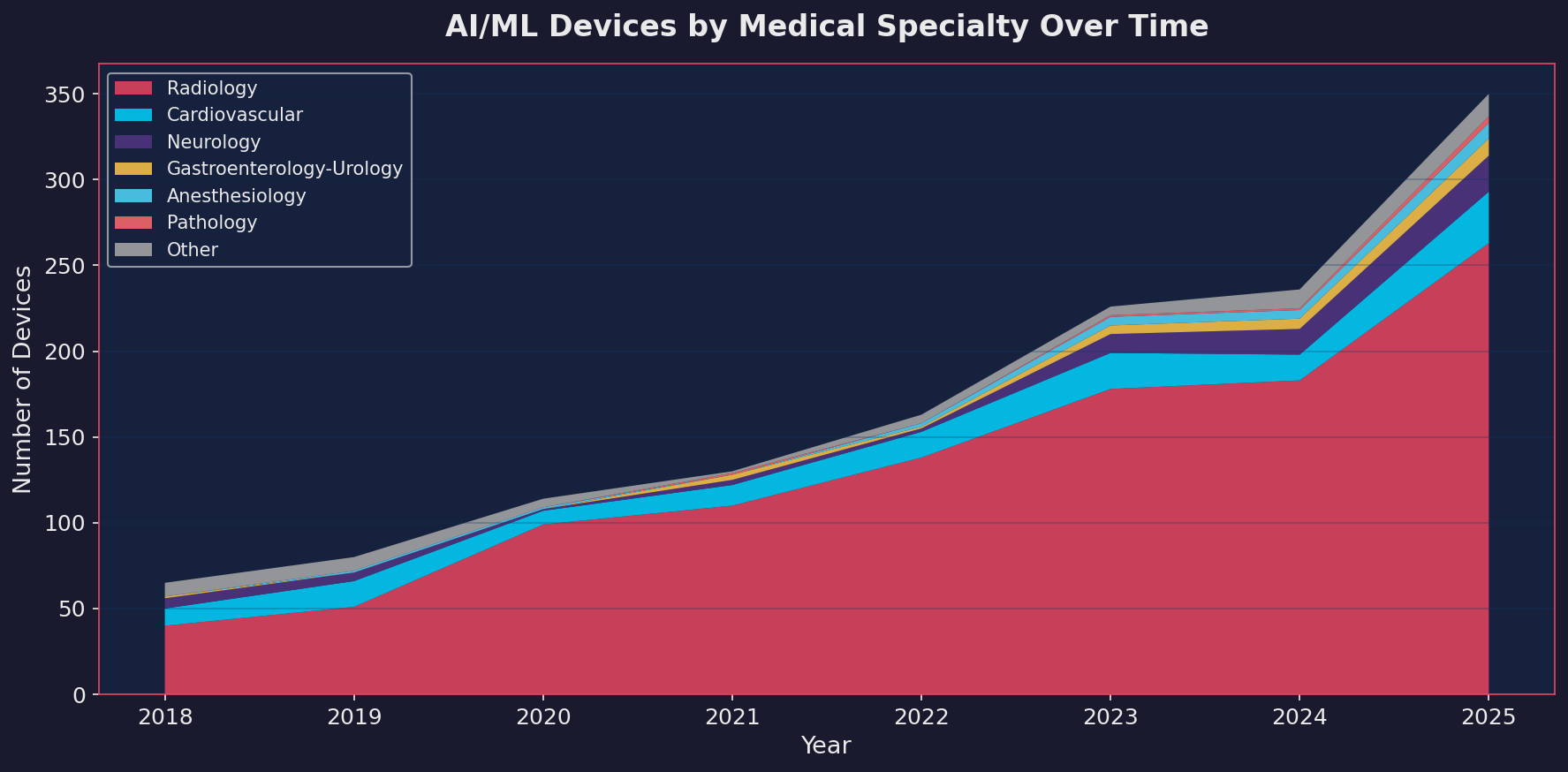

Radiology still dominates

If you’ve followed this space at all, you won’t be surprised that radiology accounts for the majority of clearances. In 2025, 263 out of 350 devices, roughly 75%, fell under the radiology panel. That’s been the pattern for years, and it makes sense. Medical imaging is where machine learning has the clearest product-market fit: large datasets, well-defined tasks, and a clinical workflow that benefits from automated triage and detection.

Cardiovascular hit 30 devices in 2025. Neurology reached 21. Gastroenterology-Urology and Anesthesiology are climbing. Pathology is small but growing. These are the specialties where the next wave is building.

Some of the most interesting 2025 clearances came from outside radiology entirely:

| Device | Company | Specialty | What It Does |

|---|---|---|---|

| Hypertension Notification Feature | Apple | Cardiovascular | Uses Apple Watch PPG data over 30-day periods to passively detect hypertension patterns. Cleared Sept 2025 via 510(k). |

| ArteraAI Prostate | Artera Inc. | Pathology | First LLM-adjacent tool authorized to prognosticate long-term prostate cancer outcomes. Uses multimodal analysis of digitized pathology slides. Cleared via De Novo. |

| Jewel Patch Wearable Cardioverter Defibrillator | Element Science | Cardiovascular | A wearable patch that detects and treats life-threatening arrhythmias. The only PMA approval in 2025. |

| Loss of Pulse Detection | Fitbit (Google) | Cardiovascular | Passive wrist-based detection of pulse loss events. |

| CHLOE BLAST | Fairtility | Obstetrics | LLM-assisted embryo assessment for IVF. |

| Gastric Alimetry | Alimetry | Gastroenterology | Body surface gastric mapping with ML analysis of gastric bioelectrical activity. |

| TriVerity | Inflammatix | Microbiology | Host-response diagnostic for distinguishing bacterial vs. viral infections. |

The Apple and Fitbit entries are worth paying attention to. Consumer wearables with FDA-cleared ML algorithms represent a fundamentally different distribution model than traditional medical devices. These aren’t sold to hospitals. They’re on millions of wrists already.

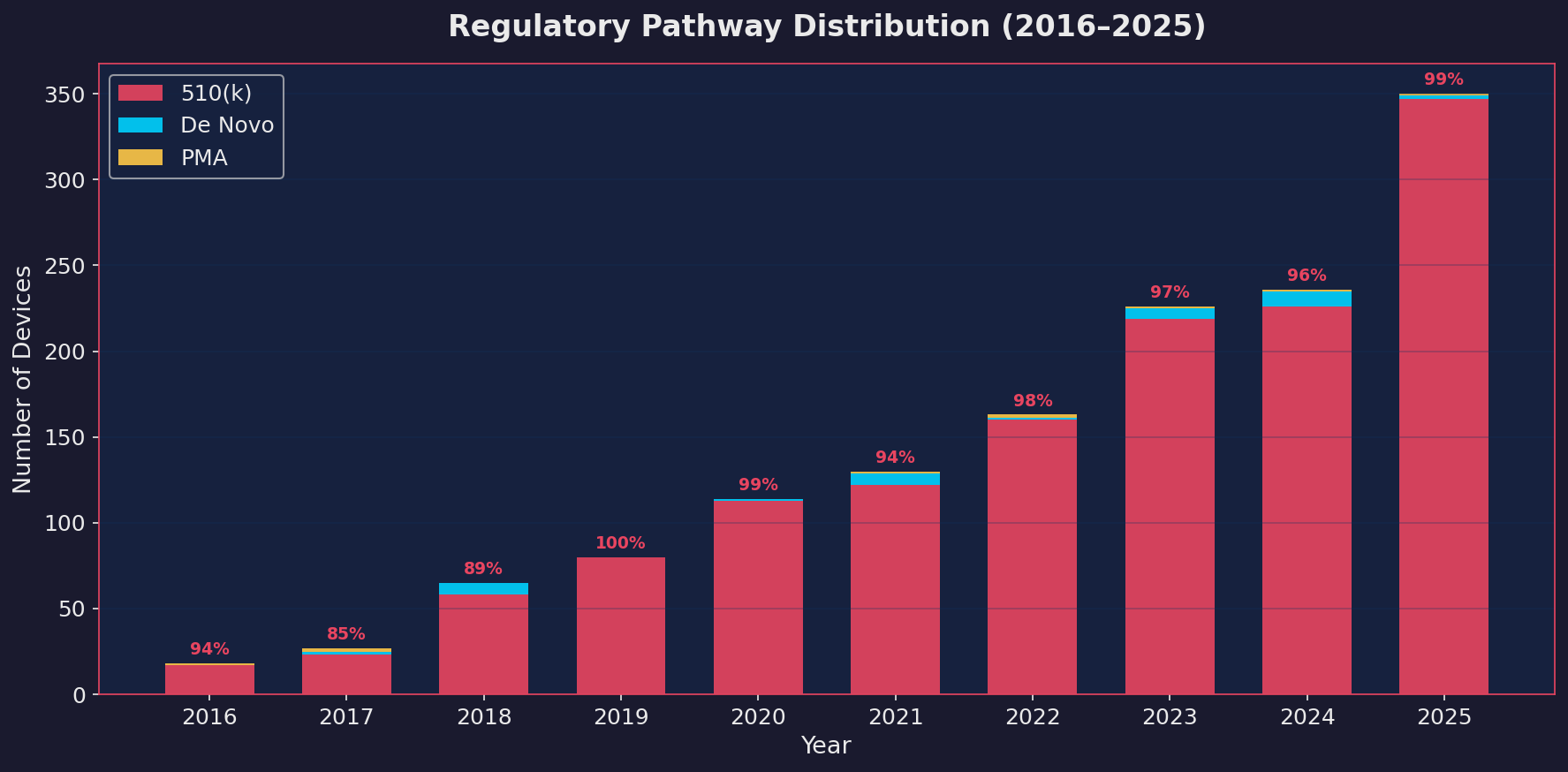

The 510(k) freeway

99.1% of all 2025 clearances went through the 510(k) pathway. Out of 350 devices, 347 were 510(k). Only 2 were De Novo. Only 1 was a Premarket Approval (PMA).

The 510(k) has been the dominant pathway since the beginning. But the concentration is getting more extreme, not less. And that tells us something important about how the FDA is actually regulating these devices.

A quick primer on the three pathways

| Pathway | What It Means | Typical Use | 2025 Count |

|---|---|---|---|

| 510(k) | Device is “substantially equivalent” to something already on the market. Fastest route, lowest evidence bar. | Most software-based diagnostic tools, imaging algorithms, triage systems | 347 |

| De Novo | Novel device with no predicate, but low-to-moderate risk. Creates a new classification that future 510(k)s can reference. | First-of-kind devices in new clinical areas | 2 |

| PMA | Highest evidence standard. Requires clinical trials demonstrating safety and effectiveness. | Life-sustaining or life-supporting devices, high-risk applications | 1 |

The reason 510(k) dominates is straightforward. Once one device in a category gets cleared, every subsequent device in that category can claim “substantial equivalence” to it and use the 510(k) pathway. The first Computer-Aided Detection (CAD) tool for mammography, the first chest X-ray triage algorithm, the first cardiac rhythm classifier: each one opened a 510(k) lane that dozens of followers now travel.

Product code QIH, which covers radiological computer-assisted diagnostic software, alone accounted for 93 of the 350 clearances in 2025. That’s a single regulatory category producing more than a quarter of all clearances. The pathway is so well-worn that companies can model their submissions on predecessors and get through in a median of about 142 days.

The De Novo gap

The two De Novo authorizations in 2025 are worth examining because they represent genuinely new categories.

ArteraAI Prostate received De Novo authorization in July 2025. It’s the first FDA-authorized tool that uses multimodal analysis of digitized H&E pathology slides to predict long-term prostate cancer outcomes and treatment response. This isn’t a radiology triage tool. It’s doing something fundamentally different: prognosticating 10-year risk of distant metastasis and predicting whether a patient will benefit from specific hormonal therapies. It was validated in Phase 3 randomized controlled trials with over 11 years of follow-up data. That’s serious clinical evidence for a software device.

Allix5 from Clairity, Inc. received De Novo authorization in May 2025 for a novel radiology application.

The most clinically ambitious applications, the ones venturing into areas where no predicate exists, face a harder regulatory path. Meanwhile, the 510(k) highway fills up with incremental variations on established themes. That’s not necessarily bad. Incremental improvements in chest X-ray triage or mammography CAD are clinically valuable. But it does mean the regulatory system favors fast followers over first movers.

If you build or regulate medical devices with machine learning components, the Predetermined Change Control Plan (PCCP) framework is the single most important regulatory development of the past two years.

The FDA finalized this guidance in late 2024, and it directly addresses a fundamental problem: machine learning models improve over time, but the traditional regulatory framework requires a new submission every time a marketed device changes significantly. That creates a perverse incentive. Companies either avoid updating their models (leaving patients with stale algorithms) or they submit dozens of 510(k)s for what are essentially version bumps.

The PCCP changes this. When a company submits a 510(k), De Novo, or PMA for a device with an LLM or ML component, they can include a PCCP that describes anticipated future modifications. If the FDA authorizes the plan alongside the device, the company can implement those pre-specified changes without filing a new marketing submission, as long as they follow the protocols laid out in the plan for data collection, validation testing, labeling updates, and cybersecurity review.

This matters great for a few reasons:

First, it acknowledges that ML-based devices are fundamentally different from static software. A traditional medical device doesn’t get better after it ships. An ML-based device can and should.

Second, it creates a framework for continuous improvement without continuous re-submission. ArteraAI’s De Novo authorization, for example, included a PCCP that allows future expansions of the tool’s capabilities without additional 510(k) submissions.

Third, and this is the part that keeps me thinking as a researcher: it puts the burden on the manufacturer to pre-specify what will change and how they’ll validate it. That’s a much harder intellectual forecasting/antcipation exercise than just submitting what you have today. You have to predict your own model’s or device’s evolution and commit to a testing protocol in advance.

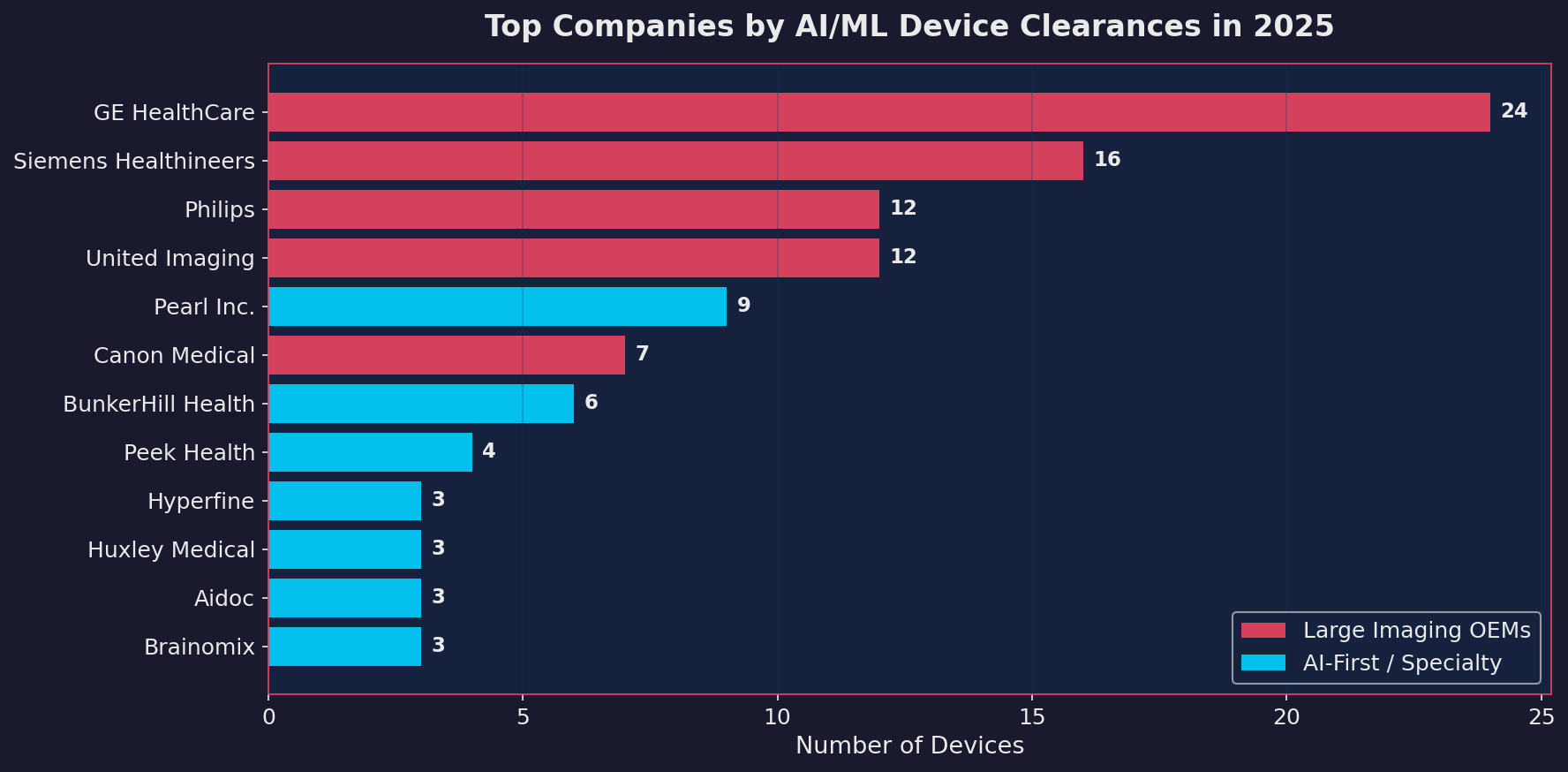

The company landscape in 2025 reveals an interesting split between legacy imaging Original Equipment Manufacturers (OEMs) and newer companies that are building ML-first.

United Imaging, a Shanghai-based company, led all manufacturers with 10 clearances in 2025. That’s notable for a Chinese company in a market where geopolitical tensions have complicated cross-border medical device approvals. Philips, Siemens, Canon Medical, and GE HealthCare all had strong showings, as expected for companies that integrate ML features into their imaging platforms.

But the more interesting story is the long tail. Companies like Pearl (dental AI), BunkerHill Health (cardiac AI), Huxley Medical (sleep diagnostics), Brainomix (stroke imaging), and Iterative Health (GI endoscopy) represent a new generation of focused ML-first medical device companies. They’re not imaging OEMs bolting AI onto existing hardware. They’re building products where the algorithm is the device.

Transformers, foundation models, and absent LLM

When people hear “AI in healthcare” in 2026, they think of ChatGPT diagnosing patients. The reality inside FDA-cleared devices is very different when we attempt to dig into the actual architectures behind these 350 devices. This turned out to be harder than expected, because the FDA doesn’t require companies to disclose their model architecture. A 2025 study in npj Digital Medicine reviewed over 1,000 FDA safety summaries and found an average transparency score of just 3.3 out of 17 for reporting model characteristics. Most submissions describe their system as “deep learning” or “machine learning” and leave it at that.

But with enough digging through 510(k) summaries, published papers, we can get a rough idea.

The CNN still leads

The vast majority of FDA-cleared devices, including the 2025 cohort, run on Convolutional Neural Networks (CNNs). ResNet, U-Net, EfficientNet, VGG. The architectures that were state of the art between 2015 and 2020.

| Device | Company | Year | Confirmed Architecture |

|---|---|---|---|

| ArteraAI Prostate | Artera Inc. | 2025 | ResNet-50 with MoCo-v2 self-supervised learning |

| AIR Recon DL | GE HealthCare | 2020+ | CNN-based MRI reconstruction |

| Viz LVO | Viz.ai | 2018 | CNN for large vessel occlusion detection |

| Paige Prostate | Paige AI | 2021 | ResNet34 multiple instance learning |

| qXR-Detect | Qure.ai | 2025 | U-Net with EfficientNetV2 backbone |

This makes sense if you think about it from a regulatory perspective. These architectures are well-characterized. Their failure modes are understood. Their behavior is deterministic: same input, same output, every time. That’s exactly what a regulator wants to see.

Here’s what I found most interesting. Transformers aren’t absent from the FDA list. They’re just not where most people are looking.

Eko EFAST (K251494, cleared August 2025) is, as far as I can determine, the first FDA-cleared device that explicitly uses a transformer-based foundation model. The name literally spells it out: “Eko Foundation Analysis Software with Transformers.” It uses a masked autoencoder framework, a self-supervised transformer architecture, pre-trained on over 4 million de-identified heart sound and ECG recordings. The underlying approach, described in a 2024 paper in npj Cardiovascular Health, learns representations from raw cardiac biosignals and then fine-tunes for specific detection tasks like murmur detection and valve disease screening.

This is not an LLM. It doesn’t generate text. It doesn’t reason or hallucinate. It’s a transformer encoder trained via self-supervised learning on domain-specific signal data, then fine-tuned for classification. But architecturally, it’s built on the same attention mechanism that powers GPT and Claude. Eko Health describes it as the first FDA-cleared foundation model for cardiovascular AI.

Aidoc’s CARE foundation model is the second strong signal. Aidoc describes CARE (Clinical AI Reasoning Engine) as a vision-language foundation model built using CT and X-ray images combined with clinical information. Their own materials reference “transformer architectures” and “attention mechanisms” explicitly. The model was trained on millions of exams and powers their BriefCase-Triage product across 11 acute indications. The January 2026 FDA clearance (K252970) makes it the first comprehensive set of double-digit indications powered by a single foundation model, achieving roughly an order-of-magnitude reduction in false alerts compared to their earlier single-condition models.

Where are the actual LLMs?

Now for the part that genuinely surprised me. Out of 1,451 FDA-cleared AI/ML devices across the entire history of the database, zero use a Large Language Model or any form of generative AI.

The RAND Forecasting Initiative has an open prediction market on whether the FDA will authorize even a single LLM-based medical device by March 31, 2026. The current crowd forecast: 2.12% probability.

The distinction matters. Eko’s EFAST uses a transformer encoder for classification. That’s architecturally related to LLMs the way a motorcycle engine is related to a jet turbine: same fundamental principles, completely different application. A transformer encoder that classifies heart sounds is deterministic, bounded, and testable. An LLM that generates free-form clinical text is stochastic, unbounded, and much harder to characterize for safety.

The regulatory challenges for actual LLMs are real:

| Challenge | Why It’s Hard |

|---|---|

| Non-determinism | Same input can produce different outputs. The FDA’s testing framework assumes reproducibility. |

| No predicate device | The 510(k) pathway needs a predicate. No LLM device exists, so the first must go De Novo. |

| Hallucination risk | A CNN produces a wrong label. An LLM produces a wrong label wrapped in a fluent, confident, medically plausible explanation. Much harder to bound the failure space. |

| Model drift | LLMs can behave differently after provider-side updates. If a device builds on a third-party LLM, an upstream update could silently change clinical behavior. |

The FDA is preparing. In mid-2025, they announced plans to identify and tag devices incorporating foundation models. In January 2025, updated Clinical Decision Support (CDS) guidance opened the door for certain LLM use cases in radiology, specifically software that analyzes a radiologist’s findings to generate proposed report summaries. And in November 2025, the Digital Health Advisory Committee held its first discussion about generative AI in mental health devices.

My prediction: the first FDA-cleared LLM-based medical device will arrive in late 2026 or 2027, likely through the De Novo pathway. It will be something narrow, a structured report generation tool or a clinical documentation assistant, rather than anything doing open-ended clinical reasoning. The transformer foundation models like Eko’s EFAST are the bridge. They prove that attention-based architectures can meet FDA standards. But the jump from transformer encoders to generative LLMs in regulated clinical use is still a large one.

Looking at this data, three trends feel inevitable:

The first: the non-radiology specialties are going to grow much faster over the next few years. Cardiology, neurology, pathology, and gastroenterology are where radiology was in 2018. The foundational work is being done now. The 510(k) predicates are being established. The flood of fast followers will come.

The second: consumer devices with FDA-cleared ML algorithms will blur the line between wellness products and medical devices in ways the regulatory framework isn’t ready for. Apple’s hypertension notification landed in a cardiovascular panel, cleared through 510(k), and shipped to millions of wrists within weeks. That’s a fundamentally different distribution model than a PACS-integrated radiology tool used by 200 hospitals.

The third: the PCCP framework will become the de facto standard for any serious ML-based medical device submission. Companies that don’t include a PCCP are essentially admitting they haven’t thought about how their model will evolve. In a field where the technology improves monthly, that’s a competitive disadvantage.

350 devices in 2025. The number will almost certainly be higher in 2026. The question isn’t whether ML is becoming standard in medical devices. That’s already decided. The question is whether our regulatory systems, our clinical validation standards, and our post-market surveillance infrastructure can keep pace with the rate at which these tools are entering clinical practice.

Based on what I’ve seen in the data, I’m not sure the answer is yes. But I’m glad someone is counting.